No Translator, No Idea, €13 Million Later

Credit professionals, curious intelectuals, and anyone tired of "top 5 stocks to watch."

I am twenty-six, standing alone in a fifteen-square-meter storeroom in the middle of nowhere, Ukraine.

In front of me: a stack of financial statements, handwritten, in a language I didn’t speak. No translator. No one else in the building...

My boss wanted my read on an agricultural company he was about to invest in— millions of euros, riding on my two-page memo, oh boy...

I didn’t know a word of Ukrainian. I didn’t know who did. I didn’t know this storeroom would become the moment that defined my future.

If I’d known, I would have run and never looked back.

I barely knew that I would end up in the murky waters of distressed debt and handle this shit for a living.

The loan that launched it

Three years later, I was on a call at 11 p.m., listening to a CFO explain why his company had six weeks of cash left — and why they needed to dilute again.

My boss had given them a loan. They didn’t pay it back. We converted it to shares. Then they kept diluting — quarter after quarter, round after round.

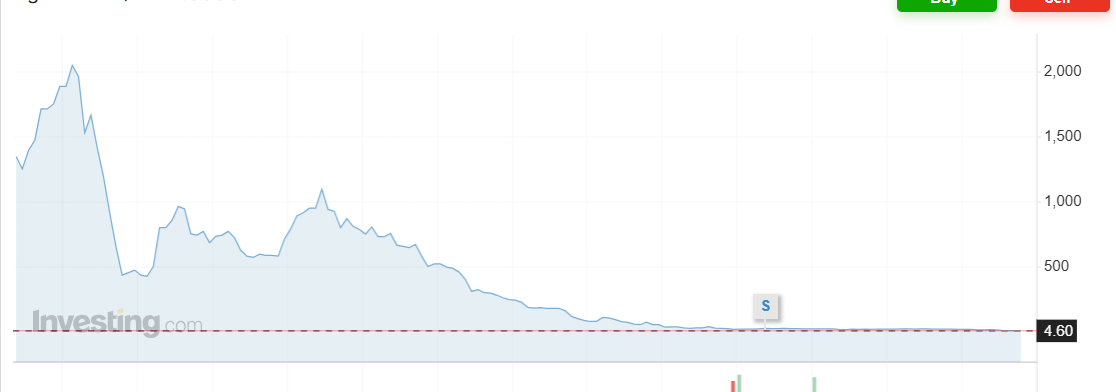

The company was listed on the Nasdaq Stockholm, running a farming business across the black earth region of Ukraine and Russia.

The market cap had been €250–300mm in the heydays. By the time we took it private, equity was worth roughly €13 million.

Over that stretch, we bought more than 10 million shares — not in one transaction, but piece by piece, collected continuously from the atomized portfolios of average retail investors. Small holdings, scattered across thousands of accounts.

Most of those owners had no idea they held the stock at all. It sat inside their retirement fund, bundled into an index allocation they'd never looked at.

But this story is not about equity or privatization. It's foundational to what corporate distressed debt actually is — a company borrows money, it can't pay it back, and the lender ends up owning what's left post restructuring.

That's the world this newsletter lives in.

Who writes this?

I’ve spent my career in distressed debt, bankruptcies, and turnarounds — with one break, for an MBA at INSEAD during COVID.

I’ve seen this from most sides: as a consultant in AlixPartners’ restructuring practice, and as an investor — institutional and individual — buying all sorts of trash.

Over the years, I moved away from corporate distress. These days I’m active in real estate-backed credit: residential and commercial NPLs, REOs, and single tickets in less crowded markets — mainly Central and Eastern Europe and the Balkans, with opportunistic shots into Western and Northern Europe.

What is here for you?

If you want daily market calls, consensus takes, or “top 5 stocks to watch,” this isn’t it — there are a thousand newsletters for that.

I also won’t publish on a fixed schedule. This business runs in waves. When the tide is out, I write what I’m living. When the tide comes in, I’m fully focused on killing the mammoth — so I have a story worth telling next time. :)

This is raw, unfiltered — thoughts as they come, they get published (with typos :().

I write about deals, underwriting, structuring, and special sits — single tickets, mostly — seen through the eyes of someone knee-deep in distressed mud, trying to survive.

This newsletter is for two types of readers:

Credit professionals who already speak the language

Curious investors — people drawn to alternative assets and the opaque world of distressed debt, alternative credit, and special situations

I still think about that storeroom sometimes.

Twenty-six, alone, no translator, a two-page memo about a sinking ship, my boss about to grant a loan of millions of euros. I had no idea what I was looking at.

Now, almost 15 years later, I’m not sure I always know either. But at least these days, when I don’t, I write about it instead of pretending I do :)

Welcome aboard.

Joe.